PVC markets across Europe have been fluctuating around record highs for months after the longest bull streak ever. Market participants are braced for fresh price spikes in November that will push the continent’s PVC market to a new high.

PVC is set to rise for 18 consecutive months

PVC prices have been on an upward trend since June 2020. This 17-month climb represents the longest bull streak in Italy since ChemOrbis began collecting. information in 2008.

The European PVC market will extend its bullish momentum into November on bullish factors including persistent shortages, higher-than-anticipated demand as well as rising raw material and utility costs. Meanwhile, ethylene contracts are expected to settle at a premium thanks to the uptrend in naphtha and spot prices. Despite initial projections of EUR 50-70/ton, market participants have shared predictions of an increase of EUR 70-90/ton in recent times.

Others have the ability to follow the discretion of Ice Cream One

Cream One is the first producer to introduce an energy surcharge of EUR 110/ton for PVC and caustic soda since October 1, and it has also taken several precautions to protect its operations due to energy costs increased sharply. A source from the manufacturer said: “Many energy-intensive companies in the thermoplastics, chemicals and metals industries have decided to reduce production capacity in order to reduce the energy bill balances they generate. I am suffering. Kem One, whose energy spending now exceeds 25% of revenue, is trying to limit its bill by reducing chlorine production as a safeguard, until energy prices return to more reasonable levels. .”

In addition to Cream One, another Western European manufacturer is considering the application of a surcharge. However, this news has not been directly confirmed by the company at the time of writing.

Suppliers may decide to raise prices above the potential increase in ethylene, due to the increase in utility costs. As a result, PVC prices could rise to triple digits next month.

Europe has yet to catch up to the price trend in other

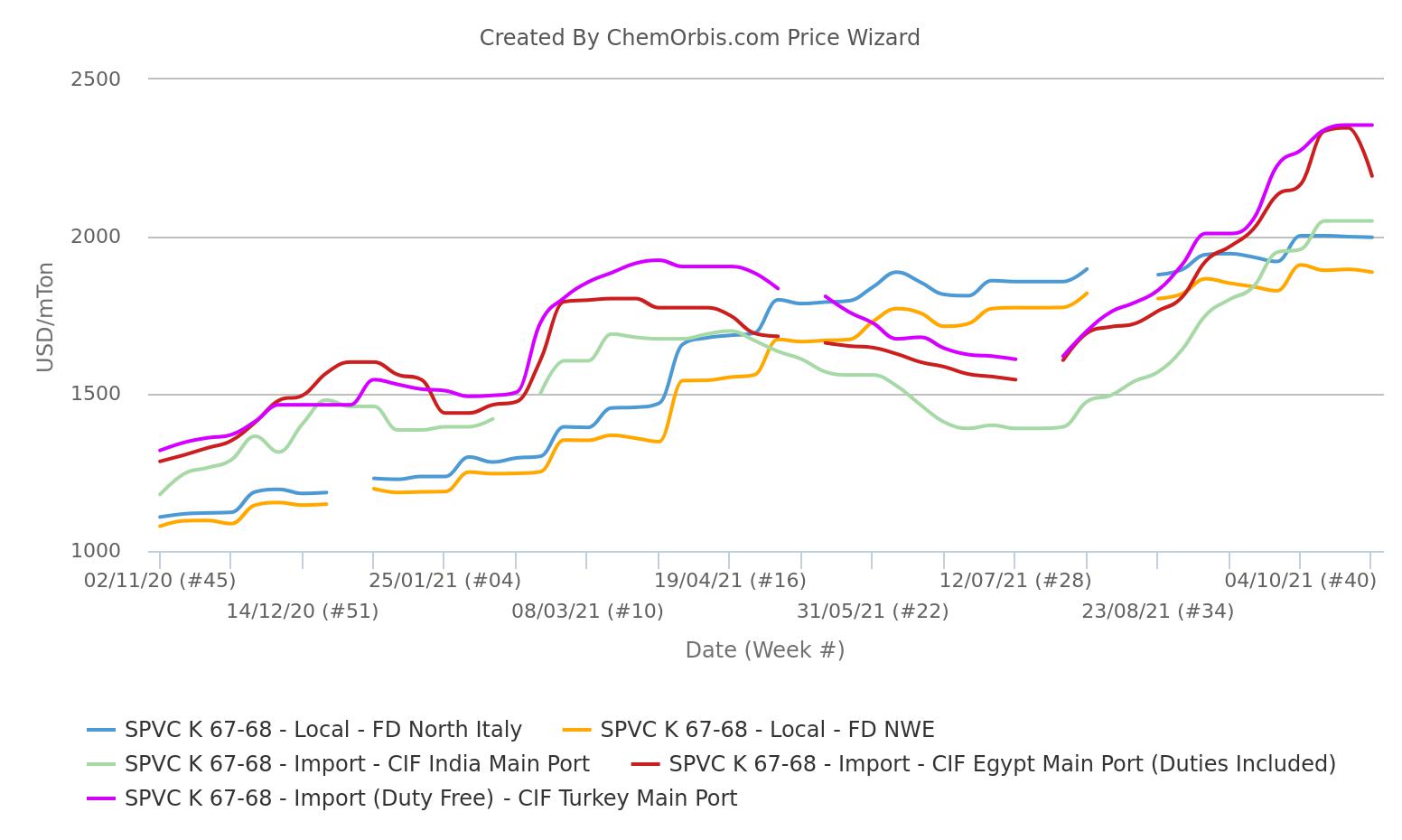

markets PVC markets in Italy and Western Europe have been left out by the uptrend in other global markets that are largely import-dependent. According to the chart below, the European market trades lower than the import markets of Turkey, India and Egypt.

According to ChemOrbis weekly average data, Europe’s premium to Turkey’s duty-free import market has increased to around $470/ton. Despite this week’s sharp downward correction, the Egyptian market for K67-68 imports is still priced at $305/ton higher than Europe, marking the biggest difference since late April. Meanwhile, Europe’s difference to India reached $165/ton.

Producers in the region think prices are still likely to go up, as European prices should be higher than other markets in equilibrium.

No relief in the near term

Supply/demand remains unbalanced as demand outstrips supply. Some European manufacturers have not yet terminated force majeure cases due to prolonged disruptions related to logistics operations or raw material procurement. While capacity in the region will partially return after the end of the maintenance, manufacturers need to rebuild inventory levels that have been low for a long time.

Buyers are said to be dependent on regional supply as import volumes are likely to remain constrained in the following months due to logistical barriers and higher margins. In fact, market participants have reported that buyers are willing to lift performance contracts as negotiations for 2022 get underway after the spot market was hit by sourcing issues. supply in 2021.

Months of backlog of orders at the finished product producer level is seen as one of the main reasons behind higher-than-expected purchase demand. Due to low inventory from manufacturers, buyers’ requests for additional volume were hardly met. It is certain that the buyer’s inventory is also decreasing due to the shortage of goods.

That means demand is likely to remain strong despite record-high prices potentially reaching another historic high in November. In the medium-term, market participants said: “If prices PVC continues to hit new highs, with some finished product manufacturers moving to other products, especially when the end customer stops buying.”